Authored by Daniel Oliver via Myrmikan Capital,

QE For The People

Myrmikan’s May letter discussed how the Fed had already begun to ease financial conditions, though the method was so subtle that few understood what the central bank was doing.

Banks are required to keep required reserves at the Fed. Banks that find themselves with a deficient reserve level have to borrow reserves from those with excess reserves, and the interest rate they pay is called the fed funds rate. The fed funds rate thereby sets the minimum level of funding for the banking system. The Federal Reserve used to set this rate through open market operations: buying Treasuries would add reserves to the banking system and lower the fed funds rate (and vice-versa).

Historically, reserves earned no interest, and so, before 2008, banks maintained as few reserves as possible—they could always buy a Treasury bill with any excess cash. After the Fed flooded the banking system with reserves during the 2008 panic, banks found themselves with excess reserves, which peaked at $2.7 trillion. The Fed sets the general reserve requirement at 10%, which means the banking system could have added $27 trillion of credit to the economy. In fact, certain classes of assets (such as Treasuries, mortgage-backed securities, etc.) have risk weightings that allow banks to hold as little as 2% reserves against them, which enables 50 times leverage on such assets (which is how, for example, Citicorp was able to be levered up 48:1 in 2007).

In order to keep trillions of levered up credit from crashing into the economy, the Fed began paying interest on excess reserves (IOER). Given the level of excess reserves, the Fed could no longer use open market operations to manipulate the fed funds rate. The Fed thought it could control the fed funds rate by manipulating IOER instead: Since Fed deposits are by definition risk-free in nominal terms, the fed funds rate should never go below IOER because if it did, banks would withdraw their loans to other banks and deposit the funds at the Fed instead. Similarly, the fed funds rate should never go above IOER because banks could withdraw reserves and lend them to other banks.

Various regulatory costs make it more expensive to lend to other banks than hold funds at the Fed, so the fed funds rate persisted roughly 0.14% below IOER (sometimes much lower) from 2009 to 2016. Yet in April 2019, the fed funds rate burst to 0.06% above IOER, or at least 0.2% above where it should have been in a smoothly functioning market. A fed funds rate above IOER means that the banks carrying $1.4 trillion in excess reserves are declining to lend them into the market to earn the spread. Myrmikan posited in April that the only reason a bank would forgo such an opportunity was that fed funds loans are unsecured and potential lenders must be worried about solvency risk—in other words the market was signalling that the banking system had solvency issues.

Events in September proved Myrmikan’s analysis to be wrong, or at least incomplete. Separate from the fed funds market is the asset repurchase market, or repo for short. The repo market is the primary funding mechanism for the shadow banking system. Repo borrowers tend to be broker-dealers, hedge funds, mortgage REITs, etc., who need short-term money to finance long-term debt (a mortgage REIT, for example, might roll 3-month repo borrowing to finance 7-year mortgage-backed security tranches). Repo lenders are entities such as banks and money market funds, who provide investors and depositors a return on their cash.

The way a repo transaction works is that the borrower agrees to sell an asset for cash and to buy it back a short while later at a tiny premium. That premium, annualized, is the repo interest rate. Only AAA-rated securities are active in the repo market, so (in theory) the lender has no risk of loss.

On September 16, the overnight repo rate exploded to a 7% premium to the fed funds market. In other words, banks were offered 7% to withdraw excess cash from their Fed accounts to lend it into the repo market. The banks’ reticence to deploy their cash cannot have been because of solvency concerns because such loans are fully secured. The only explanation is that excess bank reserves are not, in fact, excessive.

It turns out that 90% of “excess reserves” are held by just five banks, and, under Dodd-Frank, large banks must keep reserves sufficient to fund their “living will” plan of rapid and orderly resolution in case of distress. Only reserves will do, not Treasuries.

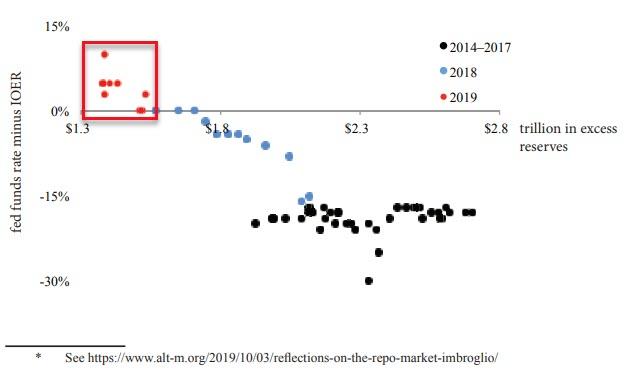

The following chart shows the growing stress in the fed funds market as the Fed engaged in quantitative tightening and reduced the amount of reserves in the banking system. This data suggests that the banking system requires at least $2 trillion of “excess” reserves to keep funding costs stable.

The part of Myrmikan’s April analysis that was wrong was the motivation of the five large banks not to lend to institutions that needed funding: it wasn’t that the banks were worried about solvency; it was that they had no cash to lend. The part of the analysis that was correct, however, is that the banking system in general, and the shadow banking system in particular, is desperate for cash and willing to pay enormous premiums to get it: the abnormal pricing in the debt markets reflects lack of liquidity, not solvency.

And this is the distinction that the banks themselves are pushing. BNP Paribas, for example, entitles a October 4 report: “LE Not QE, That’s Liquidity Expansion.” BNP predicts that the Fed will have to add $400 billion to banking reserves over the next year to eliminate banking reserve scarcity. In other words, looking at the chart above, the Fed must buy assets to try to get back to that cluster of black dots. And the only way to do that is through QE (only don’t call it QE).

Money printing has already started. In order to stabilize the $2.2 trillion repo market, on September 17 the Fed itself began lending to repo borrowers. From midSeptember through October 2, the Fed’s repo lending balance has gone from nothing to $181 billion, thereby expanding its overall balance sheet by the same amount.

There is little difference between lending funds and continually rolling them (repo) versus purchasing them outright (QE), and on October 8, Fed chairman Powell announced:

“Increasing the supply of [bank] reserves or even maintaining a given level over time requires us to increase the size of our balance sheet. As we indicated in our March statement on balance sheet normalization, at some point, we will begin increasing our securities holdings to maintain an appropriate level of reserves. That time is now upon us.”

QE is here. Trump has been proven correct once again.

The implications for gold are not obvious. Most gold investors operating under the quantity theory of money believed that QE1, QE2, and QE3 were the fuel to launch gold into the multi-thousands of dollars per ounce: more dollars meant each one was worth less, so gold had to go up. That theory proved to be incorrect in dramatic fashion. The Fed added reserves to the banking system through QE to entice banks to increase lending. Discount rates fell, asset prices increased, and more assets were constructed, increasing industrial commodity prices. Gold underperforms in real terms during a boom whatever it may do in nominal terms. Overcapacity then lowers prices, projects default, industrial commodities collapse, and gold outperforms.

This does not mean that the Fed is powerless to devalue the dollar. When the Fed buys Treasury bonds (or entices banks to do so), the government spends that money mostly as transfer payments for consumption, and few new assets are constructed. This is, in fact, an explicit strategy that Bernanke advocated in 2002:

A broad-based tax cut, for example, accommodated by a program of open-market purchases to alleviate any tendency for interest rates to increase, would almost certainly be an effective stimulant to consumption and hence to prices. … A money-financed tax cut is essentially equivalent to Milton Friedman’s famous “helicopter drop” of money. Of course, in lieu of tax cuts or increases in transfers the government could increase spending on current goods and services or even acquire existing real or financial assets.

This quotation is especially relevant because it was corporate tax payments on September 15 that led to the explosion of the repo rate: corporations wrote checks to the Treasury Department, which withdrew the money from banks, which prompted the funding stress.

Banks and shadow banks (e.g., money market funds) must have known that tax withdrawals were coming, yet they are so short of cash they had no way to prepare for it. All markets consist of a bid and an ask—therefore, one should inquire: a cash shortage compared to what demand? The larger picture is that repo borrowers have ever more assets that they must finance. Since the latest debt-ceiling compromise in July, Federal debt held by the public has soared by $517 billion. The Congressional Budget Office (CBO) projects that that figure will increase by another $758 billion by the end of 2020, by another trillion by the end of 2021, and by another $1.2 trillion in each of the next two years. And the CBO assumes real GDP growth of 2.4%. Myrmikan’s January 2019 letter points out that historical trends suggest that a recession would increase federal deficits beyond $3 trillion per year.

When the Fed lends newly-issued money into the repo market, it is effectively financing federal deficits (most of the repos are Treasuries with a smattering of mortgage-backed securities). Under the original QEs, the banking system received $2.8 trillion in new reserves and, over the ensuing decade, levered these reserves to provide $20 trillion more in credit. These QEs occurred after a credit meltdown in which the most speculative debt had been written off and during which the fed funds rate fell from 5% to 0%, making marginal projects seem profitable in the new, lower interest rate environment. The private sector thus was able to absorb half of the $20 trillion in new credit growth, and the government squirted the other half into the economy through deficit spending.

The new QE will take place near the end of a credit cycle, as overcapacity starts to bite and in a relatively steady interest rate environment. Corporate America is already choked with too much debt. As the economy sours, so too will the appetite for more debt. This coming QE, therefore, will go mostly toward government transfer payments to be used for consumption. This is the “QE for the people” for which leftwing economists and politicians have been clamoring. It is “Milton Friedman’s famous ‘helicopter drop’ of money.” The Fed wants inflation and now it’s going to get it, good and hard.

The Federal Reserve will then face the same Hobson’s choice that confronted the Reichsbank in the 1920s:

- fund the Treasury market and drive continually rising consumer inflation; or

- don’t fund it and let interest rates rise, which would crush financial markets and the economy.

QE-for-the-people is the end game of the inflationary economic cycle. Gold will anticipate it first.