T.H.E.M.

¨We believe in the judgment; we believe this first judgment will take place as God revealed, in America...¨

T.H.E.M.

¨We believe in the judgment; we believe this first judgment will take place as God revealed, in America...¨

T.H.E.M.

¨We believe in justice for all, whether in God or not; we believe as others, that we are due equal justice as human beings.¨

T.H.E.M.

¨We believe in justice for all, whether in God or not; we believe as others, that we are due equal justice as human beings.¨

Morgan Stanley Sees Recession In Three Quarters If Trade War Escalates Further

Morgan Stanley Sees Recession In Three Quarters If Trade War Escalates Further

As we await for Goldman to throw in the towel and admit its forecast of one rate hike in 2020 (and no cuts in 2019), was overly… optimistic, on Friday afternoon – with US interest rates plummeting – Barclays had a “hold my beer” moment, and just hours after JPMorgan changed its forecast as a result of an economic slowdown resulting from the escalating trade war, now expects 2 rate cuts in 2019, Barclays has one-upped the largest US bank, and revised its FOMC forecast, now expecting 3 rate cuts in 2019.

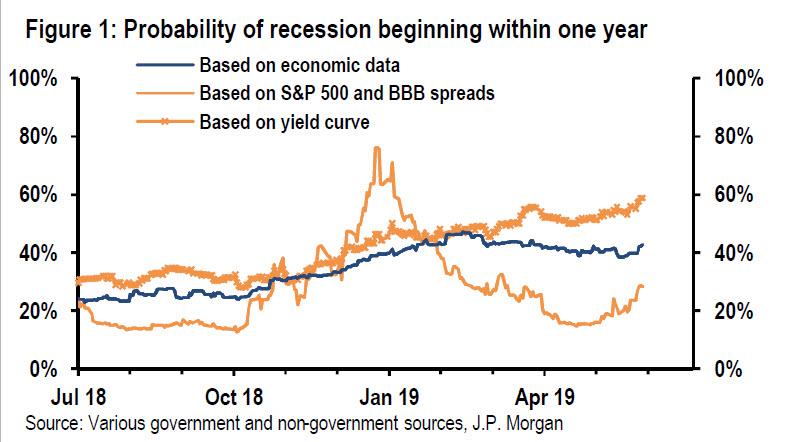

At the same time, while no bank has made a recession its base case yet, on Friday JPMorgan also updated its recession model, noting that based on the yield-curve component of its recession forecast, the probability of a recession in one year is now 60%, the highest it has been since the global financial crisis.

Now, while some may debate whether a curve inversion begins the clock on an upcoming recession, one thing is undisputible: while many analysts will caution that it is the Fed’s rate hikes that ultimately catalyze the next recession and that every Fed tightening ends with a financial “event”, the truth is that there is one step missing from this analysis, and it may come as a surprise to many that the last three recessions all took place with 3 months of the first rate cut after a hiking cycle!

In effect, what both JPM and Barclays are saying, in a politely roundabout way to avoid scaring their clients, is that the US economy is headed for a recession which incidentally is something the market has been pricing in for a while, with rates traders now anticipating at least one rate cut by the end of 2019, and three by the end of 2020.

One bank that did not lack the balls to call a spade a spade, is Morgan Stanley which over the past 6 months has emerged as Wall Street’s most bearish bank, largely thanks to the work of chief equity strategist, Michael Wilson who last week warned that the yield curve inversion is actually far more serious than apologists claim, and that as a result “volatility is about to rise a lot.”

Fast forward to today, when Wilson’s warning has spread across the bank, and in the Sunday Start note from Morgan Stanley’s Chief Economist and Global Head of Economics, Chetan Ahya, the bank goes out to warn that should Trump impose 25% tariffs on the remaining US$300 billion of imports from China and should China responding with countermeasures, “the global cycle will be at risk” and “could end up in a recession in three quarters.”

Needless to say that is nowhere near the consensus outlook, mostly because the market is still just shy of all time highs. But how is this cognitive dissonance possible?

As Ahya explains “when bad news breaks, we first react with shock, then worry about the endless possible outcomes and the time and steps needed for a complete resolution (and whether we will ever get there). However, progressive setbacks arguably cause less anxiety, even if the state of affairs is more worrisome than before. This rings true for the latest round of escalation in trade tensions, which began in early May. Tariffs have been imposed on imports from China and Mexico and the decision on imposing EU auto tariffs is delayed, not shelved, while countermeasures are being implemented by China.”

And while asset markets have moved somewhat lower, they still remain well above the levels of late last year.

This persistence in light of growing macro shocks is key. As the Morgan Stnaley economist writes, based on recent conversations with investors, he is convinced that “markets are underestimating the impact of trade tensions” and while investors are generally of the view that the trade dispute could drag on for longer, “they appear to be overlooking its potential impact on the global macro outlook.”

Needless to say, it would be remiss to underestimate this impact when the risks of tensions persisting for longer have increased. The duration and severity of the escalation will determine how it affects global growth. Given the many twists and turns in the trade talks thus far, we admit that the outcome is highly uncertain.

And, as noted above, Morgan Stanley’s worst case outcome is one where the US enters a recession in early 2020.

Here, Ahya asks rhetorically if such a prognosis alarmist? He thinks otherwise, for three reasons: (1) the transmission channels are pervasive, (2) the impact is non-linear and (3) any policy easing will be reactive, with lagged effects. Some more observations on these three points.

- The transmission channels are pervasive: Five channels will transmit trade tensions to global growth. First, implementing the tariffs will increase costs. Companies may not be able to fully pass on higher tariffs, which will erode profitability. Consumers, facing higher prices, may pull back on demand. Second, the tariffs’ impact will spill over into the domestic and global supply chains and consequently global trade flows. Third, over the medium term, multinational companies will incur additional costs as they develop alternative supply sources. Fourth, global corporate confidence will take a hit, and companies will pull back on capex, which will weigh on aggregate global demand. Finally, corporates with global footprints will face additional downward pressure on growth and profitability from their international operations. While the first three channels are probably well understood, the latter two channels, which actually have a greater impact, seem under-appreciated.

- The impact is non-linear: Moreover, as tariffs rise, the impact will be non-linear. In the first round, when 10% tariffs were imposed, the corporate sector had greater capacity to absorb them. However, if they rise to 25% and include all imports from China, corporates’ ability to absorb them will diminish, likely resulting in higher pass-throughs with more knock-on effects. In addition, as earnings growth slows and uncertainty and costs rise, the levered corporate sector will face tightening financial conditions, creating a negative feedback loop. Given higher corporate leverage, this will probably be most pronounced in the US, particularly for companies with weaker balance sheets. Against this backdrop, defaults could accelerate, bringing corporate credit risks to the fore.

- The policy response will be reactive, with lagged effects: Investors are right to expect a stronger policy response in the event of continuing escalation. However, the reality is that such policy easing will only be reactive, triggered by escalation and its effects on financial conditions and the growth outlook. What’s more, given the customary lag before policy measures impact real economic activity, a downdraft in global growth appears inevitable.

Morgan Stanley’s bottom line: “Trade tensions have re-emerged at a critical moment in the global cycle. Corporate confidence is weak, and we argue that the outcome of trade talks will be key to the global growth outlook.”

As a result, the meeting between the US and China at the G20 summit now carries an extreme level of importance because “with the latest developments suggesting that trade escalation is still in play, the impact of trade tensions on the global cycle should not be underestimated.”

ZeroHedge

Click here for reuse options!Copyright 2019 Hiram's 1555 Blog